How the Financial Picture Can Shift Over Time: We Need a Levy / No We Don't

- Amy Heutmaker

- Mar 19

- 2 min read

To help explain why financial discussions can feel inconsistent from one point in time to another, it’s useful to look at how a budget can evolve over the course of a year.

A simplified version of that process can look like this:

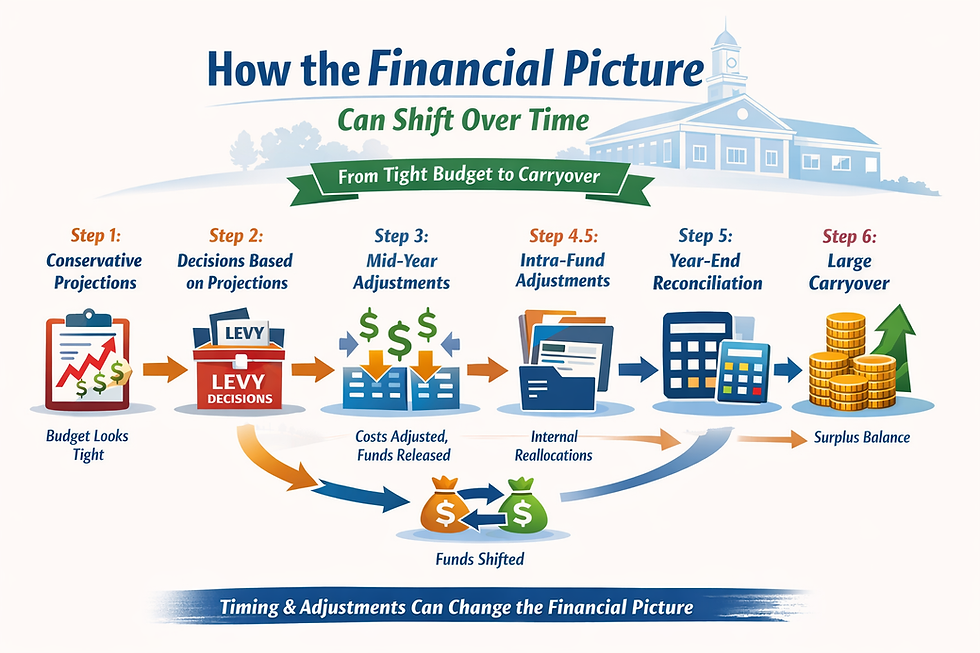

Step 1: Conservative Cost Projections. At the beginning of the budget cycle, variable expenses such as health insurance are often estimated using higher-end or “worst-case” assumptions. This is a common approach intended to avoid underfunding.

👉 At this stage, a fund may appear tight or constrained.

Step 2: Decisions Based on Projections. Those early projections are then used to inform decisions, including discussions about levies, staffing, or service levels. These decisions are made in good faith based on the information available at the time.

Step 3: Adjustments During the Year As the year progresses, actual costs begin to replace projections. In many cases, actual expenses come in lower than originally estimated. At the same time, encumbered funds (money set aside for expected expenses) may be released, and financial adjustments occur.

👉 These changes are not always immediately visible in a single snapshot.

Step 4: Interfund Support (If Needed)In some cases, funds may be supported by transfers from other sources, such as the General Fund. This is a standard tool used to maintain operations and stability.

Step 4.5: Intra-Fund Adjustments Within the Accounting System. In addition to transfers between funds, adjustments can occur within a single fund. These may include reallocating amounts between line items, releasing or modifying encumbrances, or making other internal accounting updates within the system (such as UAN).

These types of adjustments are a normal part of financial management and typically do not require formal Board action. However, because they occur within a fund rather than between funds, they can be less visible in high-level reports and may be easier to overlook without reviewing more detailed documentation.

👉 As a result, the timing and impact of these internal adjustments may not always be immediately apparent in standard budget snapshots.

Step 5: Year-End Reconciliation. Toward the end of the cycle, additional adjustments and reconciliations occur. These can include finalizing expenditures, adjusting balances, and ensuring accounts are aligned.

Step 6: Final Outcome. At the end of the year, the same fund that once appeared tight may now show a higher ending balance, often referred to as “carryover.”

Why This Matters

When viewed at a single point in time, each of these stages can present a different picture of the same fund. Without understanding the full sequence, it can be difficult to reconcile how those views connect.

That is why it is important to look not just at where a fund ends up, but how it got there. A clear understanding of timing, assumptions, and adjustments helps ensure that financial decisions are based on a complete and consistent picture.

Comments